The GSSF Standards

The Global Sustainability SyncFrame Standards are a set of universally interoperable ESG frameworks designed to help organizations, communities, and technology developers measure, manage, and improve their sustainability performance.

- Comparative Advantage

- Global Interoperability

- Integrated Sustainable Management

- Multi-faceted Materiality

- Technology as Your Ally

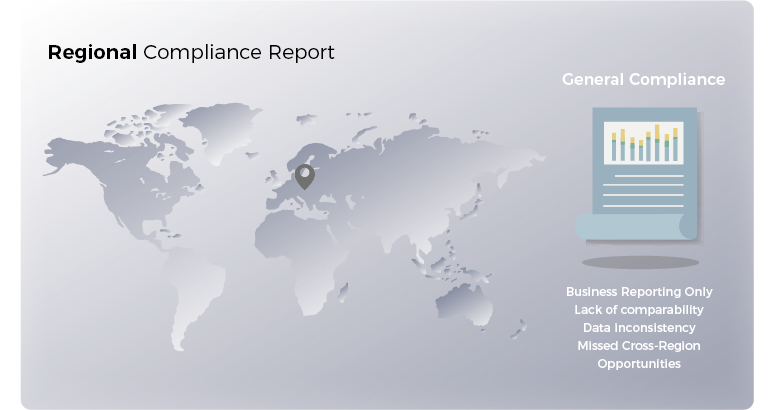

- Fragmented Standards and Complexity

- Lack of Interoperability & Comparability

- Restricted to General Business Practices

- Data Inconsistency and Limited Insights

- Missed Trans-regional Opportunities

With SyncFrame

- Global Interoperability and Strategic Alignment

- UN-Approved Partnership Engagement

- Expanded Categories for ESG Applications

- Metrics Tailored with Data Driven Insights

- Continuous Follow-up on ESG performance

Confused with ESG? Not just you. The existence of various sustainability reporting regimes across jurisdictions poses challenges for businesses, 80% of executives believe the current ESG reporting landscape is confusing.

From Fragmented Landscape to Unified Vision

As a UN-approved SDG Acceleration Action, The Global Sustainability SyncFrame provides a unified, interoperable standardization framework that integrates with global sustainability standards.

The GSSF standards simplify sustainability reporting, enabling organizations to streamline strategies across jurisdictions, reduce compliance costs, and access a broader market for their products and services.

Consistent Integration

- Auto-Sync with Proliferating Global Standards

- Benchmarking Across Sectors and Geographies

- A Common Language for ESG Reporting

Diverse Audience

- Companies & Organisations

- Communities and Policy Makers

- Technology Developers

- Financial Sectors & Investors

- Professionals and Academics

Drive Meaningful Impact

with Advanced Methodologies

Grounded in a comprehensive set of sustainability indicators, SyncFrame’s Integrated Sustainable Management framework enables organizations to implement innovative, future-proof strategies, driving sustainability goals, fostering innovation, and creating long-term value for both business and society.

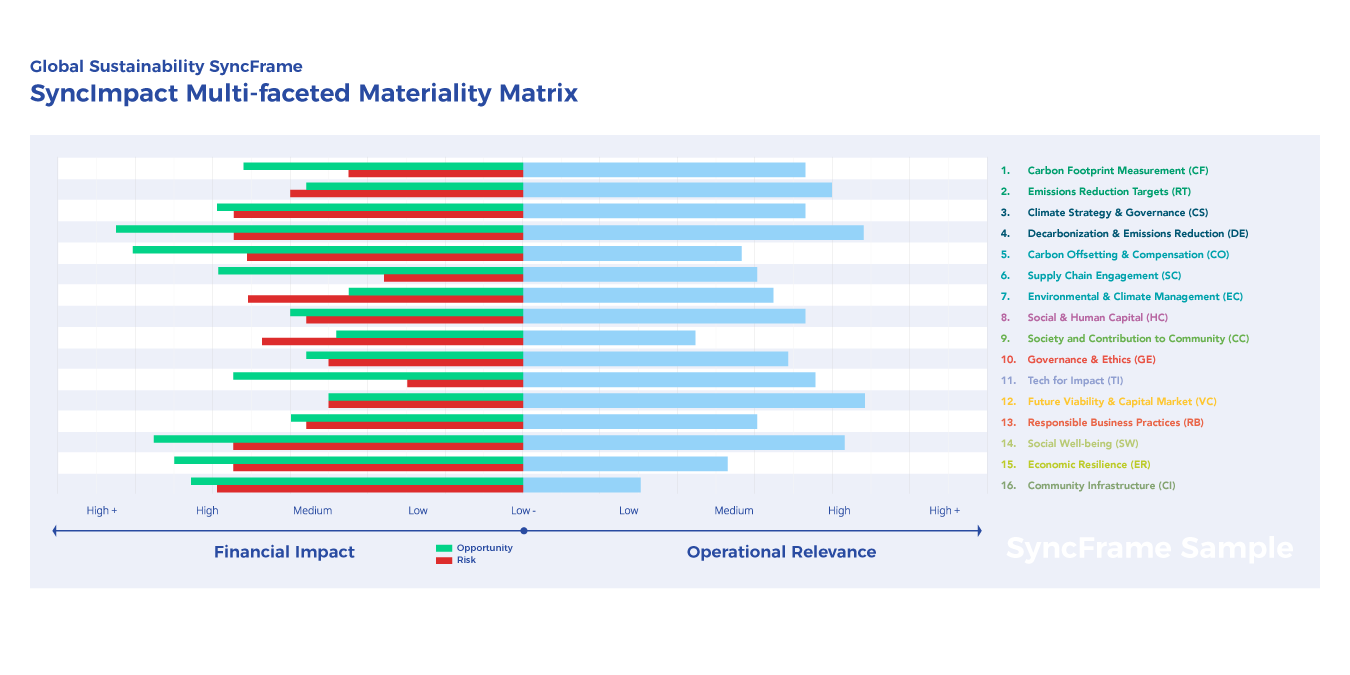

Strategic Prioritization

of ESG Issues

The SyncFrame’s Materiality Matrix is a dynamic tool that facilitates the identification and prioritization of ESG issues that are most material to an organization. Allowing organizations to:

- Plot Relevance – Assess materialities based on potential impact.

- Visualize Significance – Identify most pressing challenges & opportunities.

- Prioritize Actions: Focusing resources on greatest impact.

Innovate for Impact Merit

By incorporating advanced technology-focused metrics, SyncFrame addresses the growing need for sustainable innovation, emphasizing the role of emerging technologies in achieving long-term environmental and social objectives. This approach not only enhances the relevance and applicability of the framework but also ensures that it remains adaptable to future developments in the sustainability landscape.

Our framework incorporates technology considerations across all sustainability indicators to enhance performance and reporting.

Expanded Assessment Categories

Encapsulate environmental stewardship, social equity, governance integrity, technological innovation, and decarbonization strategies.

Assessing and improving sustainability performance across organizations.

Carbon Footprint Measurement (CF)

Indicator 1-4

Emissions Reduction Targets (RT)

Indicator 1-3

Decarbonization & Emissions Reduction (DE)

Indicator 1-2

Climate Strategy & Governance (CS)

Indicator 1-4

Environmental & Climate Management (EC)

Indicator 1-6

Social & Human Capital (HC)

Indicator 1-7

Society and Contribution to Community (CC)

Indicator 1-6

Governance & Ethics (GE)

Indicator 1-7

Evaluating technologies for their contribution to sustainability, innovation, and future viability.

Tech for Impact (TI)

Indicator 1-7

Future Viability & Capital Market (VC)

Indicator 1-7

Responsible Business Practices (RB)

Indicator 1-8

Building resilient communities and ecosystems that support sustainable living.

Environment & Climate Sustainability (EC)

Indicator 1-6

Society and Contribution to Community (CC)

Indicator 1-6

Social Well-being (SW)

Indicator 1-6

Economic Resilience (ER)

Indicator 1-8

Community Infrastructure (CI)

Indicator 1-7

Ensuring robust, transparent, and scientifically aligned strategies for achieving net-zero emissions.

Carbon Footprint Measurement (CF)

Indicator 1-4

Emissions Reduction Targets (RT)

Indicator 1-3

Decarbonization & Emissions Reduction (DE)

Indicator 1-6

Climate Strategy & Governance (CS)

Indicator 1-4

Carbon Offsetting & Compensation (CO)

Indicator 1-6

Supply Chain Engagement (SC)

Indicator 1-3

GSSF Sustainability Indicators

Version 1.0

Carbon Footprint Measurement

Indicator 1-4

SyncFrame Disclaimer

The provided sustainability indicators and disclosure specifications are intended as a general framework and may not be exhaustive. Specific requirements may vary depending on industry, jurisdiction, and individual organizational circumstances. It is essential to consult with relevant experts and regulatory bodies to ensure compliance with applicable standards and guidelines.

Interoperability with global ESG frameworks is continuously expanding as these frameworks evolve. Organizations should regularly review and update their practices to ensure alignment with the latest developments in sustainability standards.

1. Scope 1 Emissions (Direct Emissions from Owned or Controlled Sources)

Requirements:

- Measurement and Reporting: Organizations must measure and report all direct greenhouse gas (GHG) emissions from sources that are owned or controlled by the entity.

- Calculation Methodology: Use recognized protocols, such as the GHG Protocol Corporate Standard, to calculate emissions.

- Emission Factors: Apply appropriate emission factors for each type of fuel or energy source.

- Documentation: Maintain records of energy consumption, fuel usage, and other relevant data sources.

- Verification: Ensure that emissions data is independently verified by a third-party auditor.

Guidelines:

- Accuracy: Use high-quality data and robust methodologies to ensure accurate reporting.

- Boundary Setting: Clearly define the operational boundaries for emissions measurement.

- Consistency: Apply consistent calculation methods year-over-year for trend analysis.

- Transparency: Disclose assumptions, methodologies, and any exclusions in reporting.

Interoperability (Sector-Specific Frameworks):

- CDP Climate Change Questionnaire (All sectors): Align with CDP’s disclosure requirements on Scope 1 emissions.

- GRI 305-1 (General, Energy, Transport): Disclose direct GHG emissions as per the Global Reporting Initiative standards.

- GHG Protocol Corporate Standard (Scope 1): Ensure alignment with the GHG Protocol’s Corporate Standard for accounting and reporting direct GHG emissions.

- ISO 14064-1 (All sectors): Follow ISO standards for quantifying and reporting GHG emissions.

- SBTi (Science-Based Targets initiative – General, Heavy Industry, Manufacturing): Align Scope 1 emissions reporting with sector-specific decarbonization pathways.

- EU Emissions Trading System (ETS): For companies operating in the EU, ensure that Scope 1 emissions reporting aligns with requirements under the EU ETS.

2. Scope 2 Emissions (Indirect Emissions from Purchased Energy)

Requirements:

- Dual Reporting: Report both location-based and market-based Scope 2 emissions.

- Energy Consumption Tracking: Track and document all purchased electricity, heat, steam, and cooling.

- Emission Factors: Use region-specific emission factors for location-based reporting, and supplier-specific factors for market-based reporting.

- Contracts and Certificates: Disclose any energy attribute certificates (e.g., RECs) or contractual instruments used to lower market-based emissions.

- Verification: Independent verification of reported data is required.

Guidelines:

- Transparency: Clearly distinguish between location-based and market-based emissions in reporting.

- Data Sources: Use reliable data sources for electricity consumption and emission factors.

- Reconciliation: Ensure consistency between reported energy usage and emissions.

- Engagement: Engage with energy suppliers to obtain accurate emission factors.

Interoperability (Sector-Specific Frameworks):

- GHG Protocol Scope 2 Guidance: Align with the GHG Protocol’s Scope 2 Guidance for calculating and reporting indirect emissions from purchased energy.

- ISO 50001: Ensure that energy management practices align with ISO 50001 standards, which support continual improvement in energy performance.

- CDP Climate Change (C6.3): Report Scope 2 emissions in alignment with CDP’s climate change disclosure requirements.

- GRI 305-2 (General, Energy, Real Estate): Follow GRI guidelines for indirect GHG emissions.

- RE100 (Energy, Utilities): Align with RE100’s reporting standards for renewable energy use.

- ISO 14064-1 (All sectors): Adhere to ISO standards for Scope 2 emissions quantification and reporting.

- SBTi (General, Retail, Real Estate): Align with sector-specific Scope 2 reduction targets.

- IFRS Sustainability Disclosure Standards: Ensure that Scope 2 emissions are disclosed in accordance with emerging IFRS sustainability standards.

3. Scope 3 Emissions (All Other Indirect Emissions in the Value Chain)

Requirements:

- Category Reporting: Identify and report on all relevant Scope 3 categories, including upstream and downstream activities.

- Comprehensive Coverage: Cover categories such as purchased goods and services, capital goods, waste generated in operations, business travel, and product use.

- Engagement: Engage with suppliers and value chain partners to gather data.

- Methodology: Use the GHG Protocol Scope 3 Standard to guide calculations.

- Data Quality: Prioritize primary data from suppliers; use secondary data where necessary.

Guidelines:

- Prioritization: Focus on the most significant categories in terms of GHG impact.

- Improvement: Develop plans to improve data quality and coverage over time.

- Transparency: Disclose calculation methods, data sources, and any limitations.

- Aggregation: Where detailed data is unavailable, use industry averages or emission factors to estimate.

Interoperability (Sector-Specific Frameworks):

- GHG Protocol Corporate Value Chain (Scope 3) Standard: Align with the GHG Protocol’s Scope 3 Standard for accounting and reporting value chain emissions.

- CDP Climate Change Questionnaire (All sectors): Align Scope 3 disclosures with CDP requirements.

- GRI 305-3 (General, Consumer Goods, Transport): Follow GRI guidelines for value chain emissions.

- SBTi (General, Automotive, Apparel): Align with sector-specific Scope 3 targets set by the Science-Based Targets initiative.

- ISO 14044: Align with ISO 14044 standards for life-cycle assessment, particularly for product-related Scope 3 emissions.

- ISO 14064-1 (All sectors): Utilize ISO standards for reporting Scope 3 emissions.

- SASB Standards: Incorporate sector-specific guidance from SASB for reporting on value chain emissions and related risks.

4. Total GHG Emissions Intensity (Emissions per Unit of Revenue or Production)

Requirements:

- Intensity Metrics: Report GHG emissions intensity metrics such as emissions per unit of revenue, per product, or per service delivered.

- Normalization: Normalize total GHG emissions by relevant business metrics (e.g., revenue, production output).

- Sector-Specific Metrics: Choose intensity metrics relevant to the sector (e.g., emissions per ton of product for manufacturing).

- Trend Analysis: Report intensity trends over time to show progress.

Guidelines:

- Comparability: Select metrics that allow for comparison with industry peers.

- Consistency: Use the same intensity metrics year-over-year for trend consistency.

- Relevance: Ensure that the chosen metric reflects the organization’s core business activities.

- Transparency: Disclose the rationale for chosen metrics and any adjustments made.

Interoperability (Sector-Specific Frameworks):

- GHG Protocol: Align emissions intensity reporting with GHG Protocol methodologies for calculating and normalizing emissions data.

- CDP Climate Change (C7.9): Report emissions intensity metrics in alignment with CDP’s requirements, including revenue-based and production-based intensity.

- GRI Standards (GRI 305-4): Report GHG emissions intensity in accordance with GRI standards.

- SBTi (General, Cement, Chemicals): Ensure alignment with sector-specific intensity targets under the Science-Based Targets initiative.

- ISO 14064-1 (All sectors): Adhere to ISO guidelines for calculating and reporting GHG intensity.

- ISO 14067: Align with ISO 14067 standards for carbon footprinting, particularly for product-related emissions intensity.

- IFRS Sustainability Disclosure Standards: Disclose emissions intensity metrics in line with IFRS sustainability standards, ensuring consistency with financial reporting.

CF

Emissions Reduction Targets

Indicator 1-3

1. Short-term (5-10 years) and Long-term (20-30 years) Targets

Requirements:

- Quantification: Clearly define quantifiable emissions reduction targets with specific percentages or absolute reductions relative to a baseline year.

- Timeframe: Distinguish between short-term (5-10 years) and long-term (20-30 years) targets.

- Board Approval: Ensure that targets are formally approved by the organization’s board of directors or equivalent governance body.

- Public Disclosure: Disclose these targets publicly in sustainability reports, annual reports, and on the company’s website.

Guidelines:

- Scenario Analysis: Utilize climate scenario analysis (e.g., IPCC pathways) to inform the setting of targets.

- Integration with Business Strategy: Align emissions reduction targets with the overall business strategy and corporate objectives.

- Stakeholder Engagement: Engage with key stakeholders, including investors, customers, and employees, when setting and communicating targets.

- Technology Solutions: Leverage digital tools, such as AI-driven analytics, to model and optimize target scenarios.

- Review and Adjustment: Establish regular review periods (e.g., annually) to assess progress and adjust targets as necessary.

Interoperability:

- Science-Based Targets initiative (SBTi): Align targets with the SBTi criteria to ensure they are consistent with the level of decarbonization required to limit global warming to 1.5°C or well below 2°C.

- Paris Agreement: Ensure that targets contribute to the global goal of achieving net-zero emissions by mid-century, in line with the Paris Agreement.

- Task Force on Climate-related Financial Disclosures (TCFD): Align targets with the TCFD’s recommendations on scenario analysis and disclosure of climate-related risks and opportunities.

- ISO 14001: Integrate targets within the organization’s environmental management system, following ISO 14001 standards.

- GRI Standards (GRI 305-5): Disclose emissions reduction targets and performance in accordance with GRI standards for GHG emissions.

- Climate Action 100+: Align with Climate Action 100+ focus areas, particularly for companies in carbon-intensive sectors.

- UN Global Compact: Ensure targets are in line with the UN Global Compact’s principles on environmental responsibility and climate action.

- GHG Protocol: Align target setting with the Greenhouse Gas Protocol, particularly for sectors such as energy, manufacturing, and transportation.

- ISO 14064-2: For project-level GHG reductions, particularly in sectors like energy and industry.

- CDP Climate Change Questionnaire: Align disclosures with CDP’s reporting requirements.

- EU Climate Law and Taxonomy: Ensure compatibility with the European Union’s regulatory frameworks, especially for organizations operating within the EU.

2. Alignment with Science-Based Targets Initiative (SBTi) or Other Recognized Methodologies

Requirements:

- Methodological Consistency: Ensure that emissions reduction targets are consistent with methodologies recognized by the SBTi or equivalent initiatives.

- Validation: Obtain formal validation from the SBTi or similar recognized body to certify that the targets align with the goal of limiting global warming to 1.5°C or well below 2°C.

- Documentation: Maintain thorough documentation of the methodologies used to set and validate targets, including all assumptions and data sources.

Guidelines:

- Sector-Specific Pathways: Use sectoral decarbonization approaches (SDAs) where applicable, which provide sector-specific pathways aligned with climate goals.

- Data Quality: Ensure high-quality data is used in target setting, leveraging advanced data management systems and third-party verification.

- Collaboration: Collaborate with industry peers and participate in SBTi working groups to stay updated on best practices and methodological advancements.

- Technology Solutions: Implement digital platforms for tracking emissions and forecasting reductions, ensuring real-time monitoring and reporting.

- Continual Improvement: Regularly update targets to reflect the latest scientific findings and technological advancements.

Interoperability:

- SBTi Sector Guidance: For sectors like power, transportation, and real estate, use specific guidance provided by the SBTi.

- GRI Standards (Global Reporting Initiative): Align target reporting with GRI standards, particularly for disclosures related to emissions (GRI 305).

- TCFD Recommendations (Task Force on Climate-related Financial Disclosures): Ensure that climate-related targets are aligned with TCFD recommendations on governance, strategy, risk management, and metrics.

- Sectoral Decarbonization Approach (SDA): Use the SDA developed by the SBTi for sector-specific target setting, particularly for industries with unique emissions profiles.

- ISO 14064-2: Align with ISO 14064-2 for project-level emissions reductions and carbon management.

- Carbon Disclosure Project (CDP) (C4.1a): Report the alignment of targets with SBTi or other methodologies in CDP submissions.

- International Financial Reporting Standards (IFRS): Ensure that emissions reduction targets are reflected in financial disclosures and sustainability reports in line with emerging IFRS sustainability standards.

- Sustainability Accounting Standards Board (SASB): Integrate sector-specific guidance from SASB when setting and reporting on emissions reduction targets.

- Net-Zero Asset Owner Alliance (NZAOA): For financial institutions, align targets with the NZAOA framework for achieving net-zero emissions in investment portfolios.

3. Progress Towards Targets (Year-over-Year Reductions)

Requirements:

- Annual Reporting: Provide detailed annual reports on progress towards both short-term and long-term emissions reduction targets, including percentage reductions and absolute figures.

- Comparability: Use consistent metrics and methodologies year-over-year to ensure comparability of data.

- Third-Party Verification: Subject progress reports to independent third-party verification to ensure accuracy and credibility.

- Transparency: Disclose any deviations from the targets, along with explanations and corrective actions planned.

Guidelines:

- Performance Metrics: Use intensity metrics (e.g., GHG emissions per unit of production) alongside absolute emissions data to provide a more nuanced view of progress.

- Technology Integration: Utilize advanced analytics and AI tools to monitor real-time progress and predict future performance against targets.

- Communication: Regularly communicate progress to stakeholders through multiple channels, including sustainability reports, investor briefings, and digital platforms.

- Benchmarking: Compare progress against industry benchmarks to contextualize performance and drive continuous improvement.

- Risk Management: Integrate progress monitoring with enterprise risk management (ERM) frameworks to identify and mitigate risks to achieving targets.

Interoperability:

- CDP Scoring and Benchmarking: Align progress reporting with CDP’s scoring methodology to ensure comparability and recognition in global rankings.

- Task Force on Climate-related Financial Disclosures (TCFD): Disclose progress towards emissions reduction targets in line with TCFD recommendations, particularly in the context of financial risks and opportunities.

- GRI Standards (GRI 305-5): Disclose progress towards GHG emissions reduction targets in accordance with GRI standards.

- ISO 14001 and 50001: For organizations with ISO-certified environmental or energy management systems, ensure that progress tracking is integrated with these systems.

- ISO 14064-3: Align with ISO 14064-3 for the verification and validation of GHG assertions, ensuring credibility of reported progress.

- Paris Agreement Reporting: For companies with international operations, ensure that progress reporting aligns with national contributions to the Paris Agreement, particularly for companies subject to country-level reporting obligations.

- European Union Corporate Sustainability Reporting Directive (CSRD): For companies operating in the EU, ensure that progress reporting meets the disclosure requirements under the CSRD.

- Climate Action 100+: For companies targeted by Climate Action 100+, ensure that progress towards emissions reduction targets is disclosed in line with the initiative’s reporting requirements.

- UN SDG Reporting: Link progress on emissions targets with relevant Sustainable Development Goals (e.g., SDG 13: Climate Action) for broader sustainability reporting.

RT

Decarbonization & Emissions Reduction

Indicator 1-6

1. Renewable Energy Sourcing and Investment

Requirements:

- Renewable Energy Share: Specify the percentage of total energy consumption sourced from renewable sources (e.g., solar, wind, geothermal, biomass).

- Investment in Renewables: Detail investments in renewable energy infrastructure, including on-site generation and purchase agreements (e.g., Power Purchase Agreements – PPAs).

- Certification: Ensure renewable energy sourcing is certified by recognized standards (e.g., Green-e, RE100) to validate claims.

- Disclosure: Publicly disclose the renewable energy strategy, including targets, progress, and associated financial investments.

Guidelines:

- Strategic Planning: Develop a long-term renewable energy sourcing strategy that aligns with corporate sustainability goals and climate commitments.

- Technology Integration: Use digital platforms to monitor and optimize renewable energy generation and consumption in real-time.

- Diversification: Invest in a diversified mix of renewable energy sources to reduce dependency on any single energy type.

- Local Sourcing: Prioritize local renewable energy sources to reduce transmission losses and support local economies.

Interoperability:

- RE100: Align with the RE100 initiative by committing to 100% renewable electricity and publicly disclosing progress.

- Science-Based Targets initiative (SBTi): Ensure that renewable energy sourcing aligns with science-based pathways for emissions reductions.

- Task Force on Climate-related Financial Disclosures (TCFD): Disclose renewable energy sourcing in relation to climate-related risks and opportunities.

- CDP Climate Change: Align renewable energy disclosures with CDP’s climate change questionnaire (C8.2a).

- GHG Protocol: Ensure consistency with the GHG Protocol’s Scope 2 Guidance for renewable energy reporting.

- RE100 Commitment: For companies committed to 100% renewable energy, align with RE100 reporting standards.

- GRI Standards (GRI 302-1, GRI 302-4): Align with the Global Reporting Initiative’s standards for energy consumption and energy reduction.

- ISO 50001: Integrate renewable energy sourcing into the organization’s energy management system, as per ISO 50001.

- International Renewable Energy Agency (IRENA) Guidelines: Align with IRENA’s guidelines for renewable energy reporting and investment.

Technology Solutions and Approaches:

- Energy Management Systems (EMS): Implement EMS software (e.g., Energy Star Portfolio Manager, Schneider Electric EcoStruxure) to monitor and manage energy use.

- Renewable Energy Certificates (RECs): Purchase RECs to offset non-renewable energy use and support renewable energy generation.

- Power Purchase Agreements (PPAs): Engage in PPAs to secure long-term renewable energy supplies at competitive rates.

- Smart Grid Technologies: Utilize smart grid technologies to optimize renewable energy integration and improve grid reliability.

2. Energy Efficiency Initiatives Across Operations

Requirements:

- Efficiency Metrics: Define and report key performance indicators (KPIs) for energy efficiency improvements, such as energy use per unit of production.

- Implementation: Describe specific energy efficiency initiatives, such as retrofitting, equipment upgrades, and process optimization.

- Savings: Quantify energy savings achieved through efficiency initiatives in terms of absolute energy reduction and cost savings.

- Verification: Validate energy efficiency improvements through third-party audits or certifications (e.g., ISO 50001 Energy Management).

Guidelines:

- Continuous Improvement: Establish a continuous improvement process for identifying and implementing energy efficiency opportunities.

- Smart Technologies: Utilize smart meters, IoT devices, and AI-driven analytics to monitor and optimize energy use in real-time.

- Employee Engagement: Involve employees in energy efficiency programs through training and incentive schemes.

- Benchmarking: Regularly benchmark energy performance against industry standards and best practices.

Interoperability:

- ISO 50001: Align energy management systems with ISO 50001 standards for systematic energy efficiency improvement.

- GRI Standards (GRI 302-4): Align with GRI standards for reporting energy reductions and efficiency initiatives.

- EU Energy Efficiency Directive: For companies operating in the EU, ensure compliance with the EU’s Energy Efficiency Directive.

- CDP Climate Change: Report energy efficiency initiatives as part of CDP’s climate change questionnaire (C8.2).

- Task Force on Climate-related Financial Disclosures (TCFD): Integrate energy efficiency strategies into TCFD-aligned risk management and financial disclosures.

- Science-Based Targets initiative (SBTi): Ensure energy efficiency improvements are consistent with pathways to achieve science-based emissions reduction targets.

- Sustainability Accounting Standards Board (SASB): For sector-specific guidance, align energy efficiency reporting with SASB standards.

- Energy Star Guidelines: Incorporate Energy Star best practices and benchmarks for energy efficiency in buildings and facilities.

Technology Solutions and Approaches:

- Energy Management Software: Use software (e.g., Energy Star Portfolio Manager, Siemens Desigo) to track and optimize energy consumption.

- Building Management Systems (BMS): Implement BMS to automate and optimize building energy use.

- Energy-Efficient Equipment: Invest in energy-efficient lighting, HVAC systems, and industrial equipment.

- Data Analytics: Utilize data analytics tools to identify energy-saving opportunities and track efficiency improvements.

3. Electrification of Processes and Fleets

Requirements:

- Electrification Targets: Set and disclose targets for the electrification of operational processes and transportation fleets.

- Investment in Infrastructure: Detail investments in electrification infrastructure, such as charging stations, electric vehicles (EVs), and electric machinery.

- Performance Metrics: Report the percentage of electrified processes and fleet components compared to total operations.

- Environmental Impact: Assess and disclose the environmental benefits of electrification, such as reductions in Scope 1 and Scope 2 emissions.

Guidelines:

- Technology Adoption: Integrate advanced technologies, such as electric propulsion systems and battery management systems, into operations and fleets.

- Renewable Integration: Ensure that electrification is paired with renewable energy sourcing to maximize environmental benefits.

- Total Cost of Ownership (TCO): Analyze and disclose the TCO of electrification projects, including savings on fuel and maintenance.

- Partnerships: Collaborate with technology providers and energy companies to facilitate the transition to electrified operations.

Interoperability:

- GHG Protocol: Report reductions in Scope 1 emissions from fleet electrification and Scope 2 emissions from process electrification.

- CDP Climate Change: Align electrification reporting with CDP’s climate change questionnaire, focusing on emissions reductions (C8.2a).

- GRI Standards (GRI 305-1, GRI 305-2): Report electrification impacts on GHG emissions according to GRI standards.

- TCFD Recommendations: Ensure electrification strategies are integrated into TCFD disclosures on climate-related risks and opportunities.

- Science-Based Targets initiative (SBTi): Align electrification efforts with SBTi pathways for decarbonization.

- International Energy Agency (IEA): Follow IEA guidelines on electrification, particularly in sectors like transportation and industry.

- ISO 14067: Ensure that the carbon footprint of electrification initiatives aligns with ISO 14067 standards for product carbon footprints.

- Electric Vehicles Initiative (EVI): For fleet electrification, align with EVI’s global roadmap for electric mobility.

Technology Solutions and Approaches:

- Electric Vehicle Fleet Management: Implement fleet management software for electric vehicles (e.g., Geotab, Fleet Complete).

- Charging Infrastructure: Invest in electric vehicle charging infrastructure and smart charging solutions.

- Electrification Technologies: Adopt electrification technologies for processes, including electric boilers and heat pumps.

4. Carbon Capture and Storage (CCS) or Utilization (CCU) Projects

Requirements:

- Project Specifications: Provide detailed descriptions of CCS/CCU projects, including technology used, capacity, and location.

- Captured Carbon Quantification: Report the amount of CO2 captured, stored, or utilized annually, and its percentage relative to total emissions.

- Verification: Ensure that CCS/CCU projects are independently verified and compliant with recognized standards (e.g., ISO 27919-1 for CCS).

- Long-Term Storage Integrity: Disclose strategies for ensuring the long-term integrity of stored carbon, including monitoring and risk management.

Guidelines:

- Technology Readiness: Assess and disclose the technology readiness level (TRL) of CCS/CCU projects to gauge feasibility and reliability.

- Partnerships: Collaborate with research institutions, government agencies, and other stakeholders to advance CCS/CCU technologies.

- Cost-Benefit Analysis: Conduct and disclose a cost-benefit analysis of CCS/CCU projects, including potential for economic co-benefits.

- Regulatory Compliance: Ensure compliance with national and international regulations governing CCS/CCU, such as the EU’s CCS Directive.

Interoperability:

- ISO 27916: Follow ISO 27916 standards for CO2 capture, transportation, and geological storage.

- ISO 27919-1: Align CCS/CCU projects with ISO standards for carbon dioxide capture, transportation, and storage.

- GHG Protocol: Report emissions reductions from CCS/CCU under Scope 1 or Scope 3, as applicable.

- TCFD Recommendations: Integrate CCS/CCU project risks and opportunities into TCFD climate risk disclosures.

- CDP Climate Change: Disclose CCS/CCU initiatives in alignment with CDP’s climate change questionnaire (C8.2a).

- Science-Based Targets initiative (SBTi): Ensure that CCS/CCU projects contribute to meeting science-based emissions reduction targets.

- The Carbon Capture & Storage Association (CCSA): Follow CCSA guidelines for best practices in CCS.

Technology Solutions and Approaches:

- CCS Technologies: Implement advanced CCS technologies (e.g., direct air capture, post-combustion capture).

- CCU Solutions: Explore CCU technologies (e.g., carbon utilization in building materials, synthetic fuels).

- Monitoring Systems: Use monitoring systems to track and verify CO2 capture and storage effectiveness.

5. Low-Carbon Product and Service Development and Innovation

Requirements:

- Product Lifecycle Analysis: Conduct and disclose lifecycle assessments (LCA) for low-carbon products and services to quantify their environmental impact.

- Innovation Investment: Detail investments in research and development (R&D) focused on low-carbon innovations.

- Performance Metrics: Set and disclose specific metrics for low-carbon product performance, such as carbon intensity per unit of product.

- Market Impact: Report on the market adoption and impact of low-carbon products and services, including revenue from sustainable products.

Guidelines:

- Eco-Design Principles: Incorporate eco-design principles into product development to minimize environmental impact from the outset.

- Consumer Engagement: Educate consumers about the benefits of low-carbon products to drive market adoption.

- Collaboration: Partner with academic institutions, NGOs, and other companies to foster innovation and share knowledge.

- Certification: Obtain certifications for low-carbon products (e.g., Cradle to Cradle, EPEAT) to validate claims and enhance market credibility.

Interoperability:

- ISO 14040/14044: Align LCAs with ISO standards for environmental management and product lifecycle analysis.

- ISO 14067: Ensure product carbon footprint assessments align with ISO 14067 standards.

- GRI Standards (GRI 302-5): Report the environmental impact of products and services according to GRI standards.

- Carbon Disclosure Project (CDP) (C12.1): Disclose low-carbon product innovations and their impact in CDP reports.

- Sustainability Accounting Standards Board (SASB): Report on low-carbon product development in alignment with sector-specific SASB standards.

- European Union Taxonomy for Sustainable Activities: For EU-based companies, ensure that low-carbon products and services meet the criteria under the EU Taxonomy for sustainable finance.

- Science-Based Targets initiative (SBTi): Align product and service development with SBTi goals for sector-specific decarbonization.

- SBTi Criteria: Align low-carbon product development with Science-Based Targets initiative criteria where applicable.

- Cradle to Cradle Certified™ Products Program: Align product development with Cradle to Cradle principles for sustainable design.

Technology Solutions and Approaches:

- Product Lifecycle Management (PLM) Software: Use PLM software (e.g., PTC Windchill, Siemens Teamcenter) to integrate sustainability into product design.

- Life-Cycle Assessment Tools: Utilize LCA tools (e.g., SimaPro, GaBi) to evaluate and improve product environmental performance.

- Innovation Labs: Establish innovation labs to develop and test low-carbon technologies and solutions.

6. Circular Economy Practices to Minimize Waste and Emissions

Requirements:

- Circularity Metrics: Define and disclose key metrics for circular economy practices, such as material reuse rates, waste diversion rates, and emissions reductions.

- Implementation: Detail the implementation of circular economy principles in operations, including recycling, remanufacturing, and product take-back programs.

- Waste Reduction Targets: Set and disclose specific targets for waste reduction and circularity across the product lifecycle.

- Material Sourcing: Ensure that materials are sourced sustainably, with a focus on recycled and renewable inputs.

Guidelines:

- Design for Circularity: Implement circular design principles to extend product life, enhance recyclability, and reduce waste.

- Closed-Loop Systems: Develop closed-loop systems where waste materials are fully reintegrated into the production process.

- Collaboration: Work with supply chain partners to enhance circularity across the value chain.

- Technology Integration: Utilize digital tools like blockchain and AI to track and optimize circularity efforts in real-time.

Interoperability:

- ISO 14001/14044: Align circular economy practices with ISO standards for environmental management systems and lifecycle analysis.

- Ellen MacArthur Foundation: Incorporate principles from the Ellen MacArthur Foundation’s circular economy framework.

- Global Reporting Initiative (GRI) Standards (GRI 306-2): Report on waste by type and disposal method, focusing on reduction and circular practices.

- ISO 14001: Integrate circular economy practices within the environmental management system as per ISO 14001.

- Task Force on Climate-related Financial Disclosures (TCFD): Report on circular economy strategies within the broader context of TCFD-aligned climate risk management.

- Science-Based Targets initiative (SBTi): Ensure that circular economy initiatives contribute to meeting science-based emissions reduction targets.

- Carbon Disclosure Project (CDP) (C12.1): Report circular economy practices in the context of resource efficiency and waste reduction as part of CDP disclosures.

- European Union Circular Economy Action Plan: For companies operating in the EU, align with the EU’s Circular Economy Action Plan and related directives.

Technology Solutions and Approaches:

- Waste Management Systems: Implement waste management and recycling systems (e.g., Waste360, Rubicon) to track and manage waste.

- Material Recovery Technologies: Utilize technologies for material recovery and recycling (e.g., advanced sorting systems, chemical recycling).

- Circular Economy Platforms: Use digital platforms (e.g., Circulytics) to measure and optimize circularity in business operations.

DE

Climate Strategy & Governance

Indicator 1-4

1. Board Oversight of Climate Strategy and Risk Management

Requirements:

- Governance Structure: Clearly define the roles and responsibilities of the board in overseeing climate strategy, including specific committees or designated members responsible for climate-related issues.

- Regular Reporting: Ensure that the board receives regular updates on climate strategy, risk management, and performance against targets.

- Competence: Assess and disclose the climate-related expertise and training provided to board members to ensure informed decision-making.

- Accountability: Establish accountability mechanisms for board members regarding climate strategy, including performance-linked remuneration and incentives.

Guidelines:

- Integration: Embed climate considerations into the overall governance framework, ensuring that climate risks are treated with the same rigor as other material risks.

- External Advisors: Engage external experts or consultants to provide the board with up-to-date knowledge on climate risks and opportunities.

- Board Training: Implement continuous education programs for board members on emerging climate risks, regulatory changes, and best practices in climate governance.

- Stakeholder Engagement: Ensure that the board actively engages with stakeholders, including investors, on climate-related issues and integrates their feedback into strategy and decision-making.

Interoperability:

- TCFD (Governance – G1): Align disclosures with TCFD’s recommendations on board oversight of climate-related risks and opportunities.

- GRI Standards (GRI 102-18): Report on the governance structure for climate-related issues as per GRI’s General Disclosures.

- CDP Climate Change (C1): Align with CDP’s requirements on board-level oversight of climate-related issues.

- ISO 14090: Ensure that governance practices align with ISO standards on climate change adaptation, which emphasize governance as a key element.

- UN Global Compact (Principle 7): Incorporate principles related to environmental responsibility and support for precautionary approaches.

- OECD Guidelines for Multinational Enterprises: Ensure governance practices meet the OECD’s standards on environmental responsibility and corporate governance.

- EU Non-Financial Reporting Directive (NFRD): Align with NFRD’s requirements on disclosing governance related to environmental matters.

2. Integration of Climate Risk into Overall Business Strategy

Requirements:

- Risk Identification: Identify and categorize climate risks (physical, transitional, legal, reputational) and disclose their potential impact on business operations, supply chains, and markets.

- Strategic Integration: Clearly articulate how climate risks and opportunities are integrated into the company’s overall business strategy, including scenario analysis and stress testing.

- Resource Allocation: Disclose how financial and human resources are allocated to address climate risks and capitalize on climate-related opportunities.

- Performance Metrics: Establish and report on key performance indicators (KPIs) that measure the effectiveness of integrating climate risks into business strategy.

Guidelines:

- Scenario Planning: Use scenario analysis, including those aligned with a 1.5°C or 2°C pathway, to evaluate the potential impacts of climate risks on business strategy.

- Cross-Functional Teams: Create cross-functional teams that bring together expertise from finance, operations, risk management, and sustainability to ensure a holistic approach to climate risk integration.

- Resilience Building: Incorporate resilience-building measures into business strategy to adapt to both short-term and long-term climate risks.

- Communication: Ensure clear and consistent communication of the integration of climate risks into business strategy across all stakeholder communications, including annual reports and investor presentations.

Interoperability:

- TCFD (Strategy – S1, S2, S3): Align with TCFD’s recommendations on integrating climate-related risks and opportunities into overall strategy.

- CDP Climate Change (C2): Report on how climate-related risks and opportunities are integrated into your business strategy in line with CDP requirements.

- GRI Standards (GRI 201-2): Align with GRI standards on financial implications and other risks and opportunities due to climate change.

- ISO 31000: Align risk management practices with ISO 31000 standards, incorporating climate risk into enterprise risk management frameworks.

- IFRS Sustainability Disclosure Standards (S1, S2): Ensure alignment with IFRS standards on climate-related risk disclosure within the financial reporting framework.

- SASB Standards: Incorporate sector-specific guidance from SASB for integrating climate risks into business strategy and operations.

3. Engagement with Climate-Related Policy Initiatives and Advocacy

Requirements:

- Policy Participation: Disclose participation in climate-related policy initiatives, including memberships in climate-focused industry associations, and contributions to policy development.

- Advocacy Alignment: Ensure that all advocacy activities are consistent with the company’s public climate commitments and align with the objectives of the Paris Agreement.

- Transparency: Provide transparent reporting on lobbying activities, political contributions, and the alignment of these efforts with the company’s climate strategy.

- Stakeholder Collaboration: Disclose collaborations with stakeholders, including NGOs, industry groups, and governments, to advance climate policy and advocacy efforts.

Guidelines:

- Proactive Engagement: Actively engage in shaping climate-related policies that support the transition to a low-carbon economy, including providing expertise and data to policymakers.

- Internal Consistency: Ensure that internal policies and advocacy efforts are consistent with the company’s external climate commitments and public statements.

- Partnerships: Form strategic partnerships with organizations that advocate for strong climate policies and support industry-wide climate action.

- Reporting: Regularly report on the outcomes of policy engagement and advocacy activities, including the impact on the company’s climate strategy and the broader policy environment.

Interoperability:

- CDP Climate Change (C12): Align with CDP’s disclosure requirements on climate-related policy engagement and lobbying activities.

- GRI Standards (GRI 415-1): Report on political contributions and lobbying in alignment with GRI standards.

- UN Global Compact (Principle 10): Ensure compliance with the UN Global Compact principles on anti-corruption and transparent policy engagement.

- TCFD Recommendations: Integrate policy engagement activities into TCFD disclosures, particularly under the governance and strategy sections.

- OECD Guidelines for Multinational Enterprises: Align policy engagement practices with OECD’s guidelines on responsible business conduct.

- EU Corporate Sustainability Reporting Directive (CSRD): Ensure alignment with CSRD’s requirements for policy engagement and public policy advocacy disclosures.

4. Disclosure of Climate-Related Financial Risks (TCFD Recommendations)

Requirements:

- Risk Identification and Impact: Identify climate-related financial risks, including both physical and transition risks, and disclose their potential impact on financial performance and position.

- Quantitative and Qualitative Analysis: Provide both quantitative data (e.g., potential financial losses, capital at risk) and qualitative analysis (e.g., narrative on climate risk management) in disclosures.

- Alignment with TCFD: Ensure that climate-related financial disclosures are fully aligned with the four pillars of TCFD: Governance, Strategy, Risk Management, and Metrics & Targets.

- Scenario Analysis: Include scenario analysis as a key component of financial risk disclosures, outlining the assumptions, methodologies, and implications of different climate scenarios.

Guidelines:

- Materiality Assessment: Conduct a materiality assessment to determine the significance of climate-related financial risks and their relevance to stakeholders.

- Stakeholder Communication: Clearly communicate climate-related financial risks to investors, creditors, and other stakeholders through annual reports and dedicated sustainability reports.

- Third-Party Verification: Consider obtaining third-party assurance for climate-related financial disclosures to enhance credibility and stakeholder confidence.

- Continuous Improvement: Regularly update and refine financial risk disclosures to reflect new data, emerging risks, and evolving stakeholder expectations.

Interoperability:

- TCFD Recommendations: Fully align with TCFD’s recommended disclosures for climate-related financial risks across governance, strategy, risk management, and metrics.

- CDP Climate Change (C11): Ensure consistency with CDP’s requirements for disclosing climate-related financial risks and opportunities.

- GRI Standards (GRI 201-2): Align with GRI standards for reporting the financial implications of climate change.

- SASB Standards: Incorporate industry-specific guidance from the Sustainability Accounting Standards Board (SASB) for disclosing climate-related financial risks.

- EU Taxonomy Regulation: Align disclosures with the EU Taxonomy’s requirements for sustainable economic activities, focusing on climate-related risks.

- IFRS Sustainability Disclosure Standards (S2): Ensure consistency with IFRS standards on disclosing climate-related risks and opportunities.

CS

Carbon Offsetting & Compensation

Indicator 1-6

1. Quality and Verification of Carbon Offset Projects

Requirements:

- Certification Standards: Projects must be certified by reputable organizations such as Gold Standard, Verra (VCS), Climate Action Reserve (CAR), or the Clean Development Mechanism (CDM). Certification should be up-to-date and include specific details on the standards adhered to.

- Verification Reports: Provide annual third-party verification reports that detail the methodology, emission reductions achieved, and adherence to certification standards.

- Project Documentation: Disclose comprehensive project details including location, type of offset (e.g., forestry, renewable energy), emission reduction estimates, and co-benefits such as biodiversity protection.

Guidelines:

- Certification Compliance: Ensure projects meet stringent criteria for additionality, permanence, and verifiability. For instance, follow the Gold Standard’s principles or Verra’s VCS guidelines.

- Independent Audits: Conduct independent audits of offset projects every year or per the certification standard requirements to verify ongoing compliance and effectiveness.

- Stakeholder Involvement: Include local community and environmental stakeholder engagement in the offset project planning and monitoring phases.

Interoperability:

- Gold Standard: Align with Gold Standard’s requirements for project certification and monitoring.

- Verra (VCS): Follow Verra’s standards for project validation, verification, and issuance of carbon credits.

- Climate Action Reserve (CAR): Adhere to CAR standards for project validation and certification.

- Clean Development Mechanism (CDM): Align with CDM’s guidelines for project registration and verification under the UNFCCC framework.

- ISO 14064-2: Comply with ISO 14064-2 for greenhouse gas project quantification, monitoring, and reporting.

- American Carbon Registry (ACR): Align with ACR standards for project verification and carbon credit issuance.

2. Investment in Certified Carbon Offset Projects

Requirements:

- Investment Reporting: Disclose total financial investment in certified carbon offset projects annually, including the allocation to different project types and their respective certification standards.

- Portfolio Details: Provide a detailed portfolio of invested projects, including project descriptions, expected emission reductions, and the status of project certification.

- Impact Metrics: Report on impact metrics such as the amount of CO2 offset, cost per ton of CO2 reduced, and the contribution to the organization’s overall carbon neutrality goals.

Guidelines:

- Investment Diversification: Spread investments across a range of certified projects to reduce risk and enhance impact. Include projects of varying types (e.g., reforestation, renewable energy).

- Regular Impact Assessment: Periodically assess the performance of investment portfolios to ensure they meet the intended emission reduction targets and contribute to sustainability goals.

- Long-Term Commitment: Make sustained investments to support the longevity and effectiveness of offset projects.

Interoperability:

- Gold Standard and Verra (VCS): Align investments with projects certified under these standards for high-quality offsetting.

- Science-Based Targets Initiative (SBTi): Ensure investments align with science-based targets for emissions reductions.

- Global Reporting Initiative (GRI) Standards (GRI 305-4): Report investments in carbon offset projects as per GRI emissions reporting standards.

- Carbon Disclosure Project (CDP) (C10.1): Disclose investment details and their impact on carbon neutrality in CDP climate change questionnaires.

3. Transparency in Offsetting Practices and Reporting

Requirements:

- Detailed Disclosure: Provide transparent information on carbon offsetting practices, including the methodology used for offsetting, the types of projects supported, and the financial details of these investments.

- Regular Reporting: Ensure annual reporting on offsetting activities, including updates on project performance, financial investments, and emission reductions achieved.

- Audit Trails: Maintain comprehensive audit trails for offsetting practices, including documentation of verification reports and investment decisions.

Guidelines:

- Comprehensive Reporting: Ensure that all offsetting practices and results are reported in a clear, detailed, and understandable manner. Include project selection criteria and rationale for chosen projects.

- Third-Party Verification: Use independent third-party verification to enhance the credibility and transparency of offsetting practices.

- Public Access: Make offsetting reports publicly accessible to stakeholders to improve accountability and trust.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 305-5): Report on carbon offsetting practices and transparency according to GRI standards.

- Task Force on Climate-related Financial Disclosures (TCFD): Include transparency in offsetting practices in TCFD-aligned climate-related financial disclosures.

- Carbon Disclosure Project (CDP) (C10.1, C11.2): Report on offsetting practices and their impacts in CDP’s climate change questionnaire.

- ISO 14064-3: Align with ISO 14064-3 standards for the verification and validation of greenhouse gas assertions.

4. Investment in Nature-Based Solutions (e.g., Reforestation, Afforestation)

Requirements:

- Project Reporting: Disclose investments in nature-based solutions, detailing project types (e.g., reforestation, afforestation), locations, and expected carbon sequestration benefits.

- Verification: Provide evidence of third-party verification for the effectiveness of nature-based solutions, including methodologies used and the validity of carbon sequestration claims.

- Impact Metrics: Report on metrics such as the volume of carbon sequestered, improvements in biodiversity, and ecosystem restoration benefits.

Guidelines:

- Selection Criteria: Choose projects based on robust criteria for additionality and effectiveness in carbon sequestration. Ensure projects meet high environmental and social standards.

- Monitoring and Reporting: Implement comprehensive monitoring and reporting systems to track the performance and impact of nature-based solutions.

- Community Engagement: Engage with local communities to support project development and ensure long-term sustainability and benefits.

Interoperability:

- Verified Carbon Standard (VCS): Align with VCS standards for nature-based carbon sequestration projects.

- Gold Standard for the Global Goals: Follow Gold Standard’s criteria for projects focusing on climate and sustainable development goals.

- REDD+ (Reducing Emissions from Deforestation and Forest Degradation): Adhere to REDD+ guidelines for forest conservation and carbon sequestration projects.

- International Union for Conservation of Nature (IUCN): Align with IUCN’s guidelines for biodiversity and ecosystem-based projects.

5. Use of Internal Carbon Pricing Mechanisms

Requirements:

- Mechanism Disclosure: Report on the internal carbon pricing mechanisms used, including the carbon price applied per ton of CO2 and how it is integrated into decision-making processes.

- Pricing Model: Provide details on the model used for internal carbon pricing (e.g., shadow price, internal carbon fee) and its impact on financial planning and investment decisions.

- Impact Reporting: Report on the impact of internal carbon pricing on carbon reduction initiatives and overall business operations.

Guidelines:

- Transparent Application: Ensure internal carbon pricing is consistently applied across all relevant business units and operations.

- Alignment with Goals: Use internal carbon pricing to align financial incentives with sustainability goals, promoting lower-carbon investments and practices.

- Review and Update: Regularly review and adjust the carbon pricing mechanism to reflect changes in market conditions and regulatory requirements.

Interoperability:

- World Bank Carbon Pricing Dashboard: Align with the World Bank’s guidelines and dashboard for carbon pricing practices.

- Science-Based Targets Initiative (SBTi): Ensure internal carbon pricing aligns with SBTi recommendations for setting and achieving science-based targets.

- Carbon Disclosure Project (CDP) (C6.5): Disclose internal carbon pricing mechanisms and their impact in CDP reports.

- Global Reporting Initiative (GRI) Standards (GRI 207-1): Report on the use of internal carbon pricing in line with GRI’s standards for tax and economic performance.

6. Participation in Voluntary Carbon Markets

Requirements:

- Market Participation: Disclose participation in voluntary carbon markets, including the volume of carbon credits bought and sold, and the types of projects supported.

- Project Details: Report on the types of carbon offset projects supported through voluntary markets (e.g., renewable energy, forestry).

- Market Impact: Assess and report on the impact of participation in voluntary carbon markets on achieving overall carbon neutrality and meeting sustainability targets.

Guidelines:

- Credit Verification: Ensure that all credits purchased are verified by reputable standards and provide high environmental integrity.

- Market Trends: Stay updated on voluntary carbon market trends and developments to optimize participation and maximize impact.

- Stakeholder Communication: Clearly communicate the benefits and limitations of participation in voluntary carbon markets to stakeholders.

Interoperability:

- Verified Carbon Standard (VCS): Align with VCS standards for the verification and issuance of carbon credits in voluntary markets.

- Gold Standard for the Global Goals: Ensure market participation aligns with Gold Standard’s criteria for high-quality carbon credits.

- International Carbon Reduction and Offset Alliance (ICROA): Adhere to ICROA’s code of best practice for voluntary carbon market transactions.

- Carbon Disclosure Project (CDP) (C10.1): Disclose participation in voluntary carbon markets and their impacts in CDP reports.

- Climate Action Reserve (CAR): Follow CAR’s guidelines for project certification and credit issuance in voluntary markets.

CO

Supply Chain Engagement

Indicator 1-3

1. Engagement with Stakeholders on Climate Action

Requirements:

- Stakeholder Mapping: Identify and map relevant stakeholders, including suppliers, customers, community groups, and industry peers, with respect to climate action initiatives.

- Engagement Strategy: Develop and disclose a comprehensive stakeholder engagement strategy that outlines how the organization involves stakeholders in climate-related discussions and decision-making processes.

- Reporting and Feedback: Provide regular reports on engagement activities, including feedback received from stakeholders, and actions taken in response to this feedback.

- Documentation: Maintain records of stakeholder meetings, consultations, and communication strategies related to climate action.

Guidelines:

- Inclusive Approach: Ensure that stakeholder engagement processes are inclusive, transparent, and involve a diverse range of perspectives.

- Regular Communication: Conduct regular engagement sessions and updates to keep stakeholders informed about climate initiatives and progress.

- Feedback Mechanisms: Implement robust mechanisms for collecting and addressing stakeholder feedback, and demonstrate how this feedback influences climate strategies and policies.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 102-40, GRI 102-43): Align with GRI standards for stakeholder engagement and inclusivity in reporting.

- Sustainability Accounting Standards Board (SASB): Follow SASB’s guidelines for stakeholder engagement related to climate risk.

- Task Force on Climate-related Financial Disclosures (TCFD): Ensure that stakeholder engagement on climate action is included in TCFD-aligned disclosures.

- ISO 26000: Align with ISO 26000 guidance on social responsibility, particularly on stakeholder engagement.

- AccountAbility AA1000 Series: Incorporate AA1000 Stakeholder Engagement Standard (AA1000SES) for comprehensive stakeholder engagement.

2. Sustainable Procurement Practices and Supplier Codes of Conduct

Requirements:

- Procurement Policies: Develop and disclose procurement policies that incorporate sustainability criteria and address environmental and social impacts.

- Supplier Codes of Conduct: Implement and disclose a supplier code of conduct that sets clear expectations for environmental performance, ethical practices, and compliance with climate-related standards.

- Supplier Audits: Conduct regular audits and assessments of suppliers to ensure compliance with sustainability and climate-related criteria.

- Training and Capacity Building: Provide training and capacity-building programs for suppliers to improve their sustainability performance.

Guidelines:

- Criteria Integration: Integrate sustainability criteria into procurement processes, including environmental impact assessments and supplier evaluations.

- Code of Conduct Implementation: Ensure that the supplier code of conduct is enforced, with clear mechanisms for monitoring, reporting, and addressing non-compliance.

- Continuous Improvement: Regularly review and update procurement policies and supplier codes of conduct to reflect evolving best practices and regulatory requirements.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 308): Report on procurement practices and supplier environmental assessments as per GRI standards.

- Sustainability Accounting Standards Board (SASB) (EM-MU-430a.1): Follow SASB’s guidelines for sustainable procurement in specific sectors.

- ISO 20400: Align with ISO 20400 for sustainable procurement guidelines.

- B Corporation Certification: Incorporate practices and standards from B Corp certification for sustainable and ethical procurement.

- OECD Guidelines for Multinational Enterprises: Adhere to OECD guidelines on responsible supply chain management and sustainability.

3. Incentives for Suppliers to Adopt Low-Carbon Technologies and Practices

Requirements:

- Incentive Programs: Develop and disclose incentive programs aimed at encouraging suppliers to adopt low-carbon technologies and practices. Include details on the types of incentives offered (e.g., financial support, technical assistance).

- Performance Metrics: Establish and disclose performance metrics for assessing the effectiveness of incentives in promoting low-carbon technologies among suppliers.

- Success Stories: Share case studies or success stories demonstrating the impact of incentives on supplier behavior and emissions reductions.

- Monitoring and Reporting: Monitor and report on the uptake of low-carbon technologies by suppliers and the resulting environmental benefits.

Guidelines:

- Incentive Design: Design incentive programs that are aligned with overall sustainability goals and offer tangible benefits to suppliers for adopting low-carbon technologies.

- Clear Criteria: Define clear criteria for qualifying for incentives and ensure that these criteria are communicated effectively to suppliers.

- Impact Evaluation: Regularly evaluate the impact of incentive programs on supplier performance and environmental outcomes, and adjust programs as necessary to improve effectiveness.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 308-2): Report on incentives provided to suppliers for adopting sustainable practices as per GRI standards.

- Sustainability Accounting Standards Board (SASB) (EM-MU-430a.2): Align incentive programs with SASB guidelines for supplier engagement on sustainability issues.

- Task Force on Climate-related Financial Disclosures (TCFD): Include information on incentives for low-carbon technology adoption in TCFD-aligned climate-related disclosures.

- ISO 50001: Follow ISO 50001 guidelines for energy management systems, which can be integrated into supplier incentive programs.

- Science Based Targets initiative (SBTi): Align incentives with SBTi’s targets to encourage suppliers to meet science-based climate goals.

4. Technology Solutions and Approaches

- Supply Chain Management Software: Utilize software solutions that support sustainable procurement and track supplier performance against sustainability criteria (e.g., SAP Ariba, Oracle Procurement Cloud).

- Blockchain Technology: Implement blockchain technology for transparent and traceable supply chain management, ensuring compliance with sustainability standards.

- Data Analytics: Use advanced data analytics to monitor supplier performance, assess the effectiveness of incentives, and optimize procurement processes.

- Digital Platforms: Leverage digital platforms for engaging with stakeholders, providing training resources, and sharing best practices on low-carbon technologies.

SC

Environmental & Climate Management

Indicator 1-6

1. Resource Depletion and Lean Management (Business & Community)

Requirements:

- Resource Use Reporting: Disclose metrics related to resource consumption (e.g., raw materials, energy, water) and efforts to minimize resource use.

- Lean Management Practices: Report on the implementation of lean management practices aimed at reducing waste and improving efficiency.

- Resource Efficiency Metrics: Provide data on resource efficiency improvements and reductions in resource use per unit of output or revenue.

Guidelines:

- Resource Efficiency Strategy: Develop and disclose a strategy for resource efficiency, including objectives, targets, and actions.

- Lean Initiatives: Implement lean management practices such as Just-In-Time (JIT), Total Quality Management (TQM), and Six Sigma.

- Continuous Improvement: Regularly review and improve resource management practices to enhance efficiency and reduce waste.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 301-1, GRI 302-1): Report on resource use and efficiency.

- Sustainability Accounting Standards Board (SASB) (EM-MU-130a.1): Follow SASB’s guidelines for resource management and efficiency.

- ISO 14001: Align with ISO 14001 for environmental management and continuous improvement.

- Lean Enterprise Institute (LEI): Integrate best practices from LEI for lean management and resource efficiency.

Technology Solutions and Approaches:

- Resource Management Software: Use tools (e.g., SAP Integrated Business Planning, Oracle SCM Cloud) to track and optimize resource use.

- Lean Management Tools: Implement lean tools (e.g., Kanban, 5S, Value Stream Mapping) to streamline processes and reduce waste.

- IoT Sensors: Utilize IoT sensors for real-time monitoring of resource use and efficiency.

2. Energy Efficiency and Renewable Energy Integration

Requirements:

- Energy Efficiency Reporting: Disclose energy consumption metrics and improvements in energy efficiency.

- Renewable Energy Integration: Report on the integration of renewable energy sources into operations and the percentage of energy sourced from renewables.

- Investment Disclosure: Provide details on investments in renewable energy infrastructure and technologies.

Guidelines:

- Energy Efficiency Strategy: Develop and disclose a comprehensive energy efficiency strategy with specific targets and actions.

- Renewable Energy Plan: Implement a plan for integrating renewable energy sources and increasing their share in total energy consumption.

- Performance Monitoring: Regularly monitor and report on energy efficiency improvements and renewable energy integration.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 302-1, GRI 302-4): Report on energy consumption and renewable energy use.

- Sustainability Accounting Standards Board (SASB) (EM-MU-130a.2): Follow SASB’s guidelines for energy efficiency and renewable energy integration.

- ISO 50001: Align with ISO 50001 for energy management systems and continuous improvement.

- RE100 Initiative: Commit to sourcing 100% renewable electricity and report progress.

Technology Solutions and Approaches:

- Energy Management Systems (EMS): Implement EMS software (e.g., Energy Star Portfolio Manager, Schneider Electric EcoStruxure) to monitor and optimize energy use.

- Renewable Energy Certificates (RECs): Purchase RECs to offset non-renewable energy use.

- Power Purchase Agreements (PPAs): Engage in PPAs to secure renewable energy supplies.

- Smart Grid Technologies: Utilize smart grid technologies for optimizing renewable energy integration.

3. Water Usage and Conservation Efforts

Requirements:

- Water Use Reporting: Disclose total water consumption, sources of water, and water use intensity metrics.

- Conservation Initiatives: Report on water conservation initiatives and achievements, including reductions in water use.

- Water Efficiency Metrics: Provide data on improvements in water use efficiency and effectiveness of conservation measures.

Guidelines:

- Water Management Strategy: Develop and disclose a strategy for water management, including targets for reducing water use and improving efficiency.

- Conservation Practices: Implement water-saving technologies and practices, such as low-flow fixtures and water recycling systems.

- Stakeholder Engagement: Engage with local communities and stakeholders on water management and conservation efforts.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 303-1, GRI 303-3): Report on water usage and conservation efforts.

- Sustainability Accounting Standards Board (SASB) (RT-AE-140a.1): Follow SASB’s guidelines for water management and conservation.

- ISO 14046: Align with ISO 14046 for water footprint assessment.

- Water Stewardship Standard (AWS): Follow AWS guidelines for water stewardship and management.

Technology Solutions and Approaches:

- Water Management Software: Use water management software (e.g., Waterfall, Aquatic Informatics) to track and optimize water use.

- Water-Saving Technologies: Implement technologies such as rainwater harvesting systems and greywater recycling.

- IoT Sensors: Utilize IoT sensors for real-time monitoring of water use and leak detection.

4. Waste Management and Circular Economy Practices

Requirements:

- Waste Reporting: Disclose total waste generated, waste diversion rates, and types of waste managed.

- Circular Economy Initiatives: Report on initiatives to promote circular economy practices, including recycling, reuse, and material recovery.

- Performance Metrics: Provide metrics on waste reduction, recycling rates, and circularity achievements.

Guidelines:

- Waste Management Strategy: Develop and disclose a waste management strategy with specific targets for waste reduction and recycling.

- Circular Economy Integration: Integrate circular economy principles into product and process design to enhance material efficiency and minimize waste.

- Continuous Improvement: Regularly review and improve waste management practices and circular economy initiatives.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 306-2, GRI 306-4): Report on waste generation and management practices.

- Sustainability Accounting Standards Board (SASB) (EM-MU-440a.1): Follow SASB’s guidelines for waste management and circular economy practices.

- ISO 14001: Align with ISO 14001 for environmental management systems and waste reduction.

- Cradle to Cradle Certification: Evaluates waste management and circular economy practices.

- Circular Economy 100 (CE100): Includes criteria for circular economy initiatives.

- Ellen MacArthur Foundation: Integrate circular economy principles from the Ellen MacArthur Foundation.

5. Pollution Prevention and Remediation

Requirements:

- Pollution Metrics: Disclose metrics related to emissions of pollutants (e.g., air, water, and soil) and efforts to reduce pollution.

- Prevention Measures: Report on pollution prevention measures implemented and their effectiveness in reducing emissions and preventing pollution.

- Remediation Efforts: Provide information on remediation activities and outcomes for sites affected by pollution.

Guidelines:

- Pollution Prevention Strategy: Develop and disclose a strategy for pollution prevention that includes specific measures, targets, and actions.

- Compliance and Monitoring: Ensure compliance with environmental regulations and standards for pollution control. Regularly monitor and report pollution levels.

- Remediation Planning: Implement and report on plans for remediation of contaminated sites, including progress and effectiveness.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 306-1, GRI 306-5): Report on pollution emissions and remediation efforts in line with GRI standards.

- Sustainability Accounting Standards Board (SASB) (EM-MU-150a.1): Follow SASB guidelines for pollution prevention and control.

- ISO 14001: Align with ISO 14001 for environmental management systems, focusing on pollution prevention.

- Environmental Protection Agency (EPA): Adhere to EPA guidelines for pollution prevention and remediation.

- ISO 14064-2: Standards for quantifying and reporting emission reductions from pollution prevention projects.

- OECD Guidelines for Multinational Enterprises: Includes principles for pollution prevention and remediation.

6. Biodiversity Impact and Conservation Initiatives

Requirements:

- Biodiversity Metrics: Disclose metrics related to biodiversity impacts, including habitat destruction, species loss, and conservation outcomes.

- Conservation Efforts: Report on biodiversity conservation initiatives, including protected areas, species recovery programs, and habitat restoration efforts.

- Impact Assessments: Provide results from biodiversity impact assessments and their implications for business operations and conservation strategies.

Guidelines:

- Biodiversity Strategy: Develop and disclose a strategy for biodiversity conservation, including targets and actions for protecting and enhancing biodiversity.

- Impact Mitigation: Implement measures to mitigate negative impacts on biodiversity, such as habitat preservation and species protection.

- Stakeholder Engagement: Engage with stakeholders, including conservation organizations and local communities, to support biodiversity conservation efforts.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 304-1, GRI 304-4): Report on biodiversity impacts and conservation efforts according to GRI standards.

- Sustainability Accounting Standards Board (SASB) (EM-MU-160a.1): Follow SASB guidelines for biodiversity impacts and conservation reporting.

- Convention on Biological Diversity (CBD): Align with CBD principles for biodiversity conservation and reporting.

- ISO 14001: Integrate biodiversity considerations into environmental management systems per ISO 14001.

- IUCN Red List: Provide data and metrics related to species conservation and impacts.

- Forest Stewardship Council (FSC): Reporting on biodiversity impacts related to forest management.

EC

Social & Human Capital

Indicator 1-7

1. Occupational Health and Safety

Requirements:

- Health and Safety Metrics: Disclose key metrics such as the number of workplace accidents, injury rates, and absenteeism due to health issues.

- Compliance Reporting: Report compliance with local and international occupational health and safety regulations.

- Health and Safety Programs: Detail programs and initiatives aimed at improving occupational health and safety.

Guidelines:

- Health and Safety Management: Develop and implement a health and safety management system with clear policies, procedures, and responsibilities.

- Risk Assessment: Regularly conduct risk assessments to identify and mitigate workplace hazards.

- Training and Awareness: Provide ongoing training and awareness programs for employees on health and safety practices.

Interoperability:

- Global Reporting Initiative (GRI) Standards (GRI 403-1, GRI 403-2): Reporting on occupational health and safety practices and performance.

- Sustainability Accounting Standards Board (SASB) (CG-CH-320a.1): Guidelines for health and safety metrics and management.

- ISO 45001: Align with ISO 45001 for occupational health and safety management systems.

- Occupational Safety and Health Administration (OSHA): Follow OSHA guidelines for workplace safety.